Finding affordable health insurance in the United States without employer coverage can be challenging, but there are several options that provide meaningful protection without high costs. Whether you are self-employed, between jobs, part-time, or do not receive insurance through an employer, you can still find plans that fit your budget and health needs.

This guide explains the most accessible options for affordable health insurance in the USA without employer coverage, how to compare plans, and tips to choose the best fit in 2026.

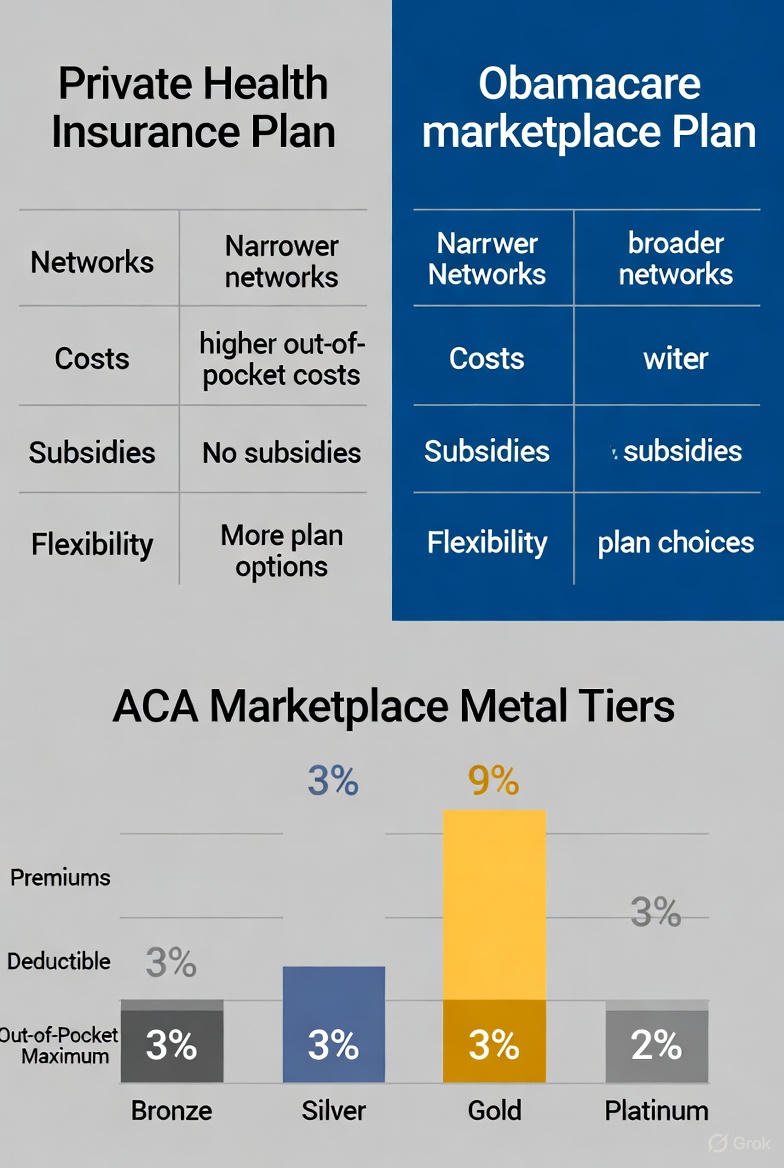

Health Insurance Marketplace Plans

The health insurance marketplace is a government-supported platform where individuals and families can buy coverage directly. These plans are designed to provide essential health benefits, including doctor visits, hospital care, prescription drugs, preventive services, and emergency care.

Marketplace plans come in different levels that affect how much you pay monthly and when you use services. The levels include Bronze, Silver, Gold, and Platinum. Bronze plans tend to have lower monthly payments but higher costs when you access care. Silver and Gold plans balance monthly costs and out-of-pocket expenses.

Many people choose marketplace plans because they offer structured coverage and financial support based on income.

Subsidies and Financial Assistance

Low-cost health insurance often becomes more affordable with financial help. Subsidies are available to people who qualify based on income and household size. These subsidies reduce monthly payments and can lower overall costs.

When you apply for marketplace coverage, the income information you provide determines whether you qualify for subsidies. The result can be a significant reduction in the cost of health insurance.

Medicaid and CHIP

For people with low income, government programs such as Medicaid and the Children’s Health Insurance Program (CHIP) offer low-cost or no-cost coverage. Eligibility for these programs depends on income and state of residence, as rules vary across the country.

Medicaid provides health coverage for adults and children in many low-income families, while CHIP focuses on children in families that do not qualify for Medicaid but still need affordable coverage.

Short-Term Health Insurance

Short-term health insurance plans provide temporary coverage when you need protection for a limited period. These plans often have lower monthly costs than full marketplace plans. However, short-term plans may not cover all benefits and may exclude pre-existing conditions.

Short-term health insurance can work as a stop-gap solution while you transition between long-term plans, but it is important to understand what is and is not covered.

High Deductible Health Plans and Health Savings Accounts

High Deductible Health Plans have lower monthly premiums and higher deductibles. These plans can be an affordable choice for people who are generally healthy and do not anticipate frequent medical needs.

Paired with a Health Savings Account, high deductible plans offer tax-advantaged ways to save for medical expenses. Contributions to a Health Savings Account reduce taxable income, and the funds can be used to pay qualified medical costs.

Popular Affordable Plan Providers

Many health insurance companies offer affordable plans that can be purchased without employer coverage. The availability and cost of these plans vary by state and individual needs.

Some providers focus on budget-friendly plans in the marketplace, including options that emphasize preventive care, telehealth access, and wellness support. Plans vary in network size, covered services, and pricing, so comparing options is important.

Tips for Choosing Affordable Health Insurance

Choosing the right affordable health insurance plan requires understanding your health needs and comparing multiple factors.

Consider how often you visit doctors, whether you take prescription medications, and whether you expect major medical care. Plans with low monthly costs may require higher payments when you use services, so balancing premium and out-of-pocket costs is key.

Make sure the plan’s provider network includes doctors and hospitals you prefer. Out-of-network care usually costs more.

Look beyond monthly premiums and compare deductibles, copayments, coinsurance, and maximum out-of-pocket costs. A plan with slightly higher monthly payments can cost less overall if it has lower out-of-pocket expenses.

Understanding what services are covered, such as preventive care, prescription drugs, mental health services, and telehealth options, helps you choose a plan that delivers meaningful value for your health and budget.

Enrollment Periods

Affordable health insurance plans are usually available during the annual open enrollment period. If you miss this time frame, you may still enroll if you experience qualifying events such as marriage, birth of a child, or loss of previous coverage.

Understanding the enrollment rules helps you avoid gaps in coverage.

Common Questions

How do subsidies work for people without employer coverage?

Subsidies reduce monthly payments and are determined by income and family size when applying through the health insurance marketplace.

Are short-term plans a good choice for long-term coverage?

Short-term plans can be more affordable, but they may not offer comprehensive protection and may exclude pre-existing conditions.

Can I change plans any time?

Most plans can only be changed during open enrollment, unless you experience a qualifying life event.

Conclusion

Affordable health insurance in the USA without employer coverage is achievable through marketplace plans, subsidies, government programs, short-term options, and high deductible plans with health savings accounts. By comparing plan levels, costs, and benefits, individuals and families can find coverage that protects their health and financial wellbeing in 2026.