Choosing health insurance in the United States can be confusing, especially when comparing private health insurance and Obamacare (Affordable Care Act Marketplace plans). Both options provide ways to get coverage, but they work differently and may be better suited for different people. This guide explains the core differences, benefits, drawbacks, costs, and which choice might be best based on your needs.

What Is Private Health Insurance?

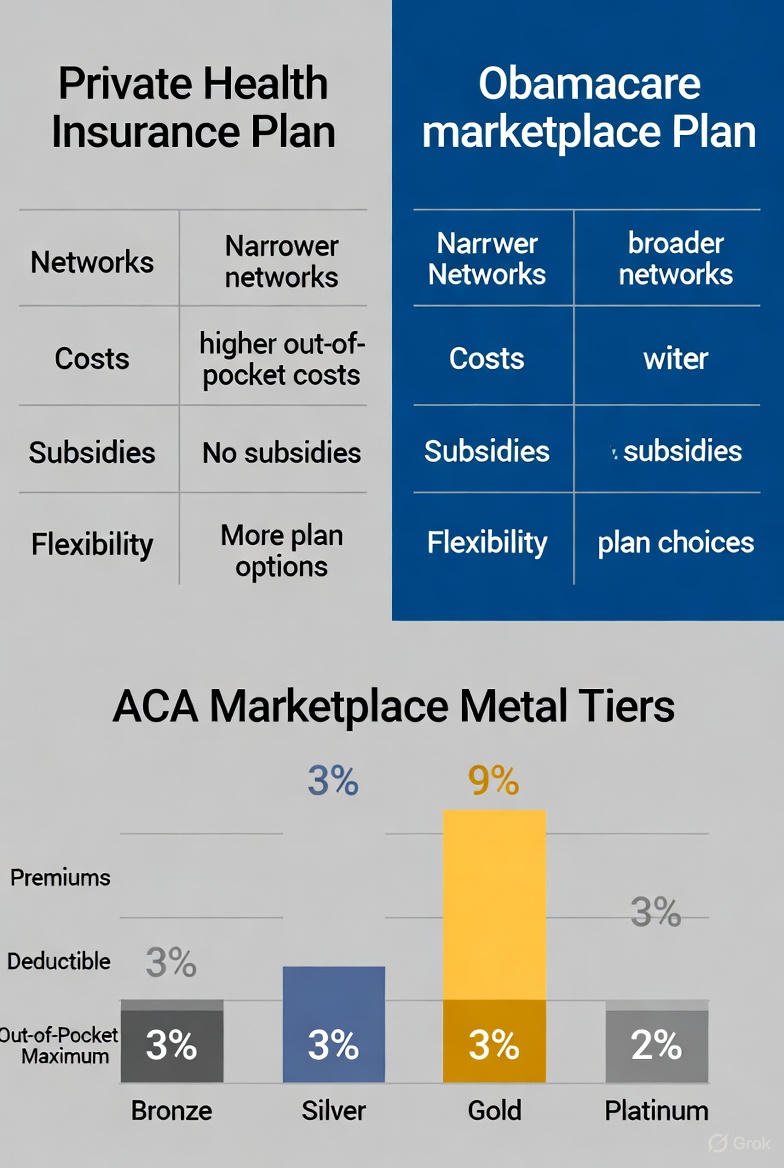

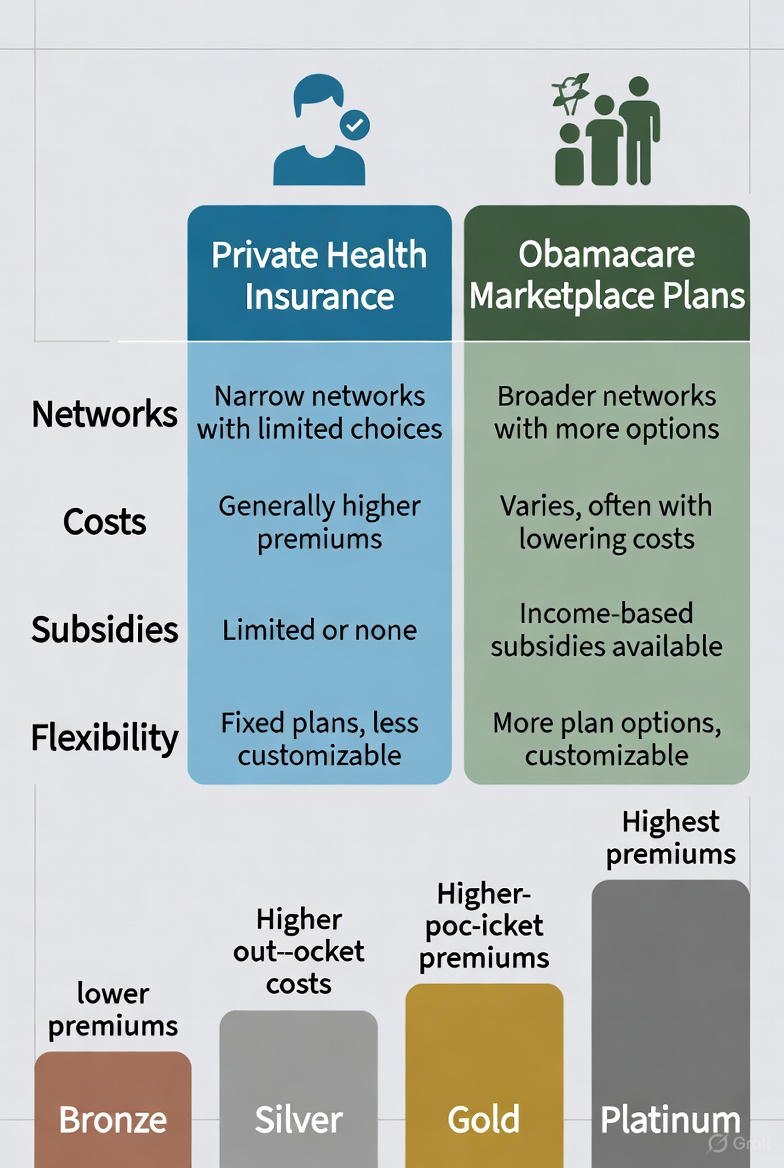

Private health insurance is a policy you buy directly from an insurance company or through a broker. These plans are not part of the government-run marketplace but are sold in the open market. You can choose from many private companies and customized plan options.

Private insurance plans vary widely in coverage, price, network size, benefits, and rules.

What Is Obamacare (Marketplace) Health Insurance?

Obamacare refers to health insurance plans available through the Affordable Care Act (ACA) marketplace. These plans are regulated by federal law and must meet certain standards, including covering essential health benefits like preventive care, hospital visits, and prescriptions.

Marketplace plans are grouped into levels (Bronze, Silver, Gold, Platinum) based on how costs are shared between you and the insurer.

Subsidies may be available based on income, which can significantly reduce your monthly premium or out-of-pocket costs.

Key Differences

Eligibility and Access

Private Plans:

-

Anyone can buy private insurance at any time in most cases

-

No income limits or eligibility requirements based on income

-

Not subject to open enrollment restrictions in the same way Marketplace plans are

Obamacare (Marketplace) Plans:

-

Available only during open enrollment or after a qualifying life event

-

Subsidies are income-based, so only people within certain income ranges qualify

-

Plans must follow ACA rules

Cost and Financial Assistance

Private Plans:

-

Monthly premiums can be higher

-

No government subsidies are available

-

Costs vary widely based on the insurer, plan type, age, location, and health status

Obamacare Plans:

-

Subsidies may reduce monthly premiums if you qualify based on income

-

Cost-sharing reductions may lower deductibles and other out-of-pocket costs

-

Premium costs are more predictable because they are standardized within metal tiers

Coverage Requirements

Private Plans:

-

Coverage requirements depend on the plan and state laws

-

Plans may not cover all essential health benefits that ACA plans must include

Obamacare Plans:

-

Must cover essential health benefits such as hospital care, prescriptions, maternity care, mental health services, and preventive care

-

Cannot discriminate based on pre-existing conditions

Network Access and Flexibility

Private Plans:

-

Can offer broader or narrower provider networks depending on the insurer

-

Some plans let you see out-of-network doctors for an additional cost

Obamacare Plans:

-

Also have network restrictions, but plans must offer adequate provider access in your area

-

You may find more standardized networks with ACA plans

Pros and Cons

Pros of Private Health Insurance

-

Greater flexibility to choose plans year-round

-

Usually more varied plan options

-

Can be easier to get customized coverage

-

Sometimes better for people who do not qualify for subsidies

Cons of Private Health Insurance

-

Higher overall costs

-

No income-based assistance

-

Coverage may not include all essential health benefits

-

Private plans may be harder to compare because they vary widely

Pros of Obamacare Marketplace Plans

-

Financial help available through subsidies

-

Covers essential health benefits

-

Cannot deny coverage based on pre-existing conditions

-

Annual spending limits help protect against high costs

Cons of Obamacare Marketplace Plans

-

Must enroll during open enrollment or after a qualifying event

-

Networks may be limited

-

Income requirements apply for financial help

-

Costs can still be high without subsidies

Who Should Choose Private Health Insurance?

Private health insurance may be better if:

-

You do not qualify for ACA subsidies due to higher income

-

You need coverage outside of the open enrollment period

-

You want a plan with specific benefits not offered on the marketplace

-

You prefer a custom plan through a broker

Who Should Choose Obamacare Marketplace Plans?

Marketplace (Obamacare) plans may be better if:

-

You qualify for income-based subsidies

-

You want coverage that includes essential health benefits

-

You prefer predictable cost structures and federal consumer protections

-

You want protection against denial for pre-existing conditions

Cost Comparison

The cost of health insurance varies widely depending on age, location, plan type, and personal health. Subsidized marketplace plans can often be cheaper than private plans for people with moderate or low income.

In contrast, private plans without subsidies may be more expensive overall, especially for comprehensive coverage.

Coverage Quality and Benefits

Obamacare plans must follow federal rules that guarantee minimum coverage standards. This means you can expect coverage for essential services such as preventive care, doctor visits, hospital stays, prescription drugs, maternity care, and mental health services.

Private plans may offer similar benefits, but coverage levels can vary. Some private plans offer more flexibility, while others may limit services to reduce cost.

Network and Provider Access

Both private and marketplace plans use provider networks. A broader network gives you more choices for doctors and hospitals. Before choosing a plan, check whether your preferred providers are in the network.

Out-of-network care is usually more expensive in both private and marketplace plans.

Enrollment Periods and Timing

Marketplace plans are subject to open enrollment windows. If you miss open enrollment, you can enroll only if you have a qualifying life event such as job loss, marriage, or birth of a child.

Private plans often allow enrollment year-round, though plan availability and prices can change.

Making the Right Decision

The best choice depends on your situation:

-

Evaluate your income and eligibility for subsidies

-

Compare total costs including premiums, deductibles, and out-of-pocket limits

-

Consider your need for flexibility and timing

-

Check provider networks and covered benefits

Comparing plans side by side helps you decide which option is better for your health needs and budget.

Conclusion

Private health insurance and Obamacare marketplace plans both provide ways to get health coverage in the USA, but they serve different needs. Private plans offer flexibility and variety, while marketplace plans provide federal consumer protections and financial help for eligible individuals and families.

Your best choice depends on your income, coverage needs, timing, and whether you qualify for subsidies. By understanding the differences, you can choose a plan that best fits your health requirements and financial situation in 2026.