Full coverage car insurance is a popular option for drivers in the United States who want comprehensive protection for their vehicles and themselves. Unlike minimum liability insurance, full coverage combines multiple types of protection to cover a wider range of risks. This guide explains what full coverage includes, factors affecting cost, average rates in 2026, and tips to save on premiums.

What Is Full Coverage Car Insurance?

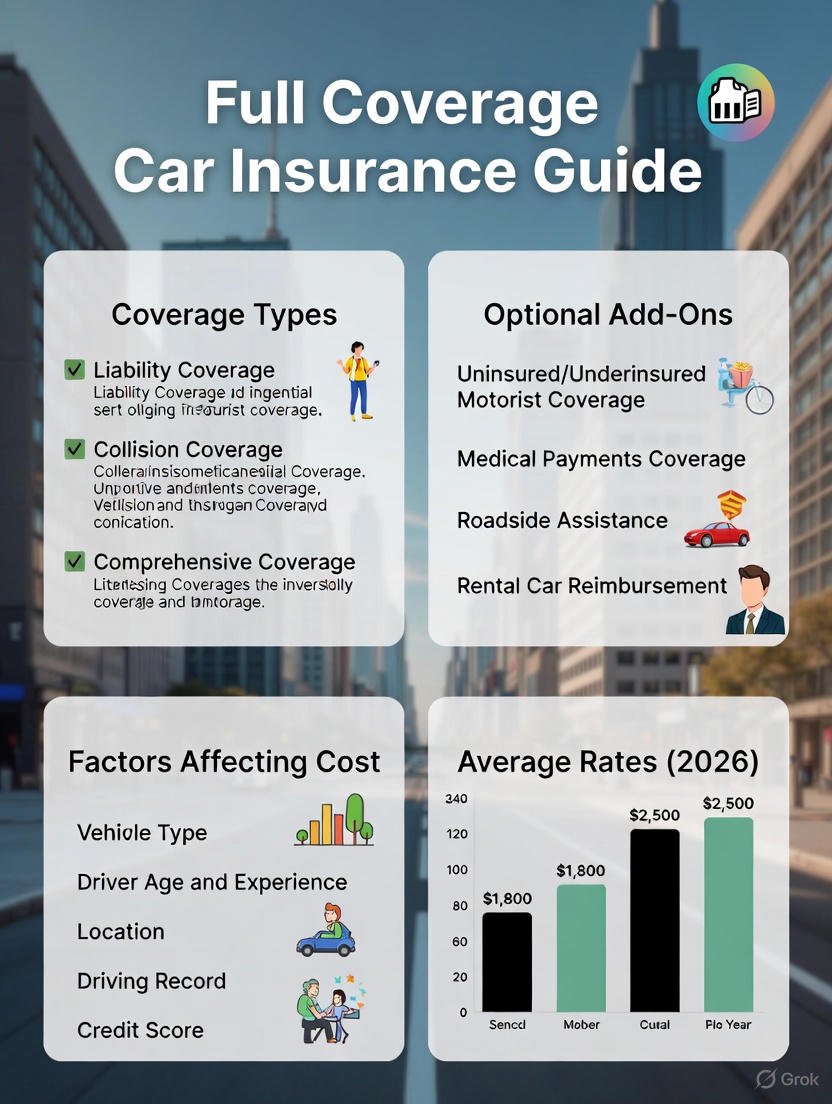

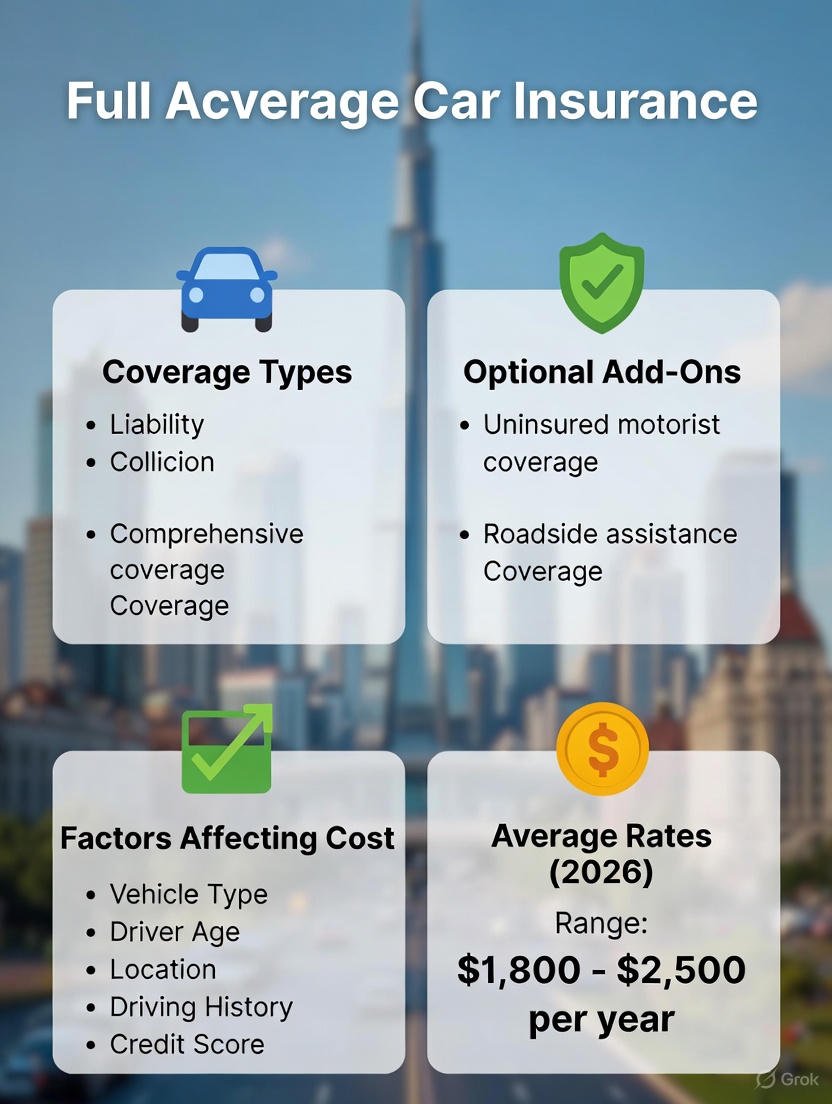

Full coverage car insurance generally refers to a combination of liability, collision, and comprehensive coverage. It is not a specific policy, but rather a term used to indicate broader protection than minimum state requirements.

-

Liability coverage – Pays for damages or injuries you cause to other people or property.

-

Collision coverage – Pays for damage to your car after an accident, regardless of who is at fault.

-

Comprehensive coverage – Covers damage to your vehicle from non-collision events like theft, vandalism, fire, natural disasters, and falling objects.

Full coverage may also include optional add-ons, such as:

-

Uninsured/underinsured motorist coverage – Protects you if the other driver has little or no insurance.

-

Personal injury protection (PIP) – Covers medical expenses for you and your passengers.

-

Roadside assistance – Helps with towing, battery jumps, and flat tires.

-

Rental car reimbursement – Covers the cost of a rental car while your vehicle is being repaired.

Who Needs Full Coverage?

Full coverage is recommended for drivers who:

-

Own a newer or expensive vehicle

-

Have a car loan or lease (lenders often require full coverage)

-

Want maximum financial protection in case of accidents or damage

-

Live in areas with higher risk of theft, vandalism, or severe weather

Drivers with older, low-value cars may choose to drop collision and comprehensive coverage to save money, depending on the vehicle’s worth.

Factors That Affect Full Coverage Cost

The cost of full coverage car insurance varies based on several factors:

-

Vehicle type – Luxury or high-performance cars cost more to insure.

-

Driver age and experience – Younger or new drivers pay higher premiums.

-

Location – Urban areas with heavy traffic or high crime rates generally have higher rates.

-

Driving record – Accidents or traffic violations increase premiums.

-

Credit history – In some states, credit affects insurance pricing.

-

Coverage limits and deductibles – Higher limits and lower deductibles increase cost.

Optional add-ons such as roadside assistance or rental car coverage also increase premiums.

Average Cost of Full Coverage in 2026

Full coverage car insurance is more expensive than minimum liability coverage because it offers broader protection. While rates vary by state, vehicle, and driver profile, national averages for 2026 show:

-

Full coverage – $1,800 to $2,500 per year for a typical driver

-

Liability-only coverage – $600 to $900 per year

-

High-risk drivers – Full coverage can exceed $3,000 per year

Drivers with clean records, safe driving habits, and discounts may pay less than the average.

How to Get the Best Rates on Full Coverage

Compare Multiple Quotes

Shop around and compare full coverage quotes from at least three different insurers. Coverage and pricing can vary widely.

Increase Deductibles

Choosing a higher deductible lowers your premium. Make sure you can afford the deductible if you need to file a claim.

Ask About Discounts

Many insurers offer discounts for:

-

Safe driving

-

Good students

-

Multi-policy bundling (home and auto)

-

Anti-theft devices

-

Low mileage

Drive a Safe Vehicle

Cars with good safety ratings, lower repair costs, and anti-theft features often qualify for lower rates.

Maintain a Clean Driving Record

Avoiding accidents and traffic violations over time helps reduce premiums.

Benefits of Full Coverage Car Insurance

-

Comprehensive protection – Covers a wide range of risks beyond basic liability.

-

Financial security – Reduces out-of-pocket expenses after accidents or theft.

-

Peace of mind – Provides confidence that your vehicle and finances are protected.

-

Lender compliance – Required if you have a car loan or lease.

Potential Drawbacks

-

Higher premiums – Full coverage costs more than minimum insurance.

-

Depreciation factor – If your car is older, paying full coverage may not be cost-effective.

-

Optional coverage may be unnecessary – Some add-ons might not be needed for all drivers.

Popular Full Coverage Auto Insurance Providers in the USA

Some leading insurers that offer full coverage include:

-

State Farm – Wide network, multiple discounts, reliable claims service

-

GEICO – Competitive rates, user-friendly online tools

-

Progressive – Flexible plans, usage-based programs for safe drivers

-

Allstate – Many add-ons like accident forgiveness and roadside assistance

-

USAA – Highly rated for military members and families

Comparing coverage options and quotes from multiple companies helps find the best balance of cost and protection.

Conclusion

Full coverage car insurance in the USA provides peace of mind and comprehensive protection for drivers who want to safeguard their vehicles and finances. While it costs more than minimum liability coverage, the benefits often outweigh the expense, especially for newer or valuable cars.

By understanding what full coverage includes, how costs are calculated, and strategies to lower premiums, drivers can make informed decisions in 2026 and choose a policy that meets both their protection needs and budget.