Being self‑employed gives freedom, but finding the right health insurance can be confusing. Unlike employer plans, self‑employed individuals must choose and manage their own coverage. Affordable and quality health insurance is important to protect against rising medical costs and unexpected health needs. This article explains the best health insurance options for self‑employed people in the USA in 2026, how to choose plans, and tips to save money.

Why Health Insurance Matters for Self‑Employed People

Self‑employed workers do not have employer‑provided health insurance. Without coverage, medical bills can be costly and difficult to manage. A good health insurance plan provides:

-

Coverage for doctor visits and hospital stays

-

Preventive care

-

Prescription drug benefits

-

Financial protection against large medical expenses

Affordable and reliable insurance can improve peace of mind and overall financial stability.

Affordable Health Insurance Options for the Self‑Employed

Self‑employed individuals have multiple options to find health insurance coverage. Each option has different costs, benefits, and eligibility rules.

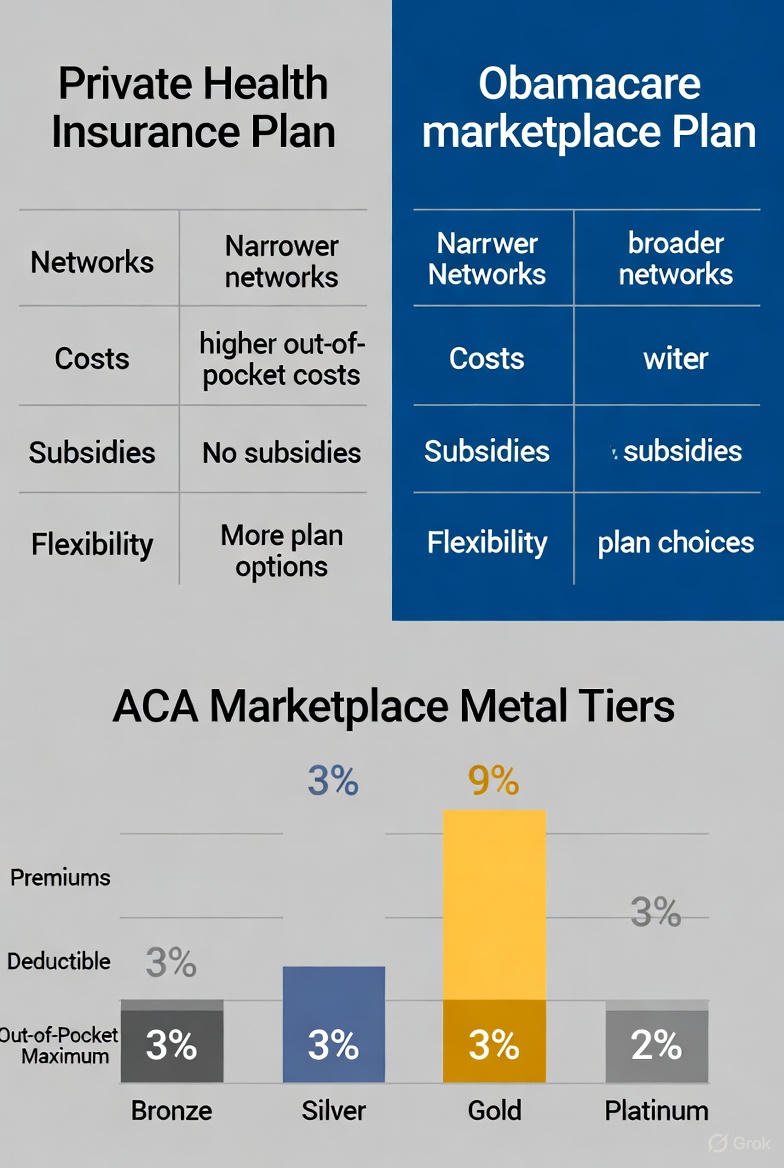

Health Insurance Marketplace Plans

The health insurance marketplace is a common choice for self‑employed people. Plans are available through federal or state exchanges. These plans are often called ACA or marketplace plans.

Marketplace Plan Levels

Marketplace plans are grouped into four main tiers:

-

Bronze

-

Silver

-

Gold

-

Platinum

Bronze plans usually have lower monthly premiums but higher out‑of‑pocket costs. Silver and Gold plans balance monthly cost and coverage. Platinum plans offer higher coverage with higher premiums.

Marketplace plans often cover essential health benefits such as doctor visits, emergency care, prescription drugs, and preventive services.

Subsidies and Cost Assistance

Self‑employed individuals may qualify for premium subsidies based on income. Subsidies can significantly reduce the monthly cost of health insurance. Eligibility for subsidies depends on household income and family size. Subsidies help make plans more affordable for many self‑employed people.

Subsidies are available when buying coverage through the health insurance marketplace. It is important to enter accurate income information to determine eligibility for cost assistance.

Short‑Term Health Insurance

Short‑term health insurance plans can be a low‑cost option for temporary coverage. These plans are often used by people between jobs or waiting for long‑term coverage to begin. Short‑term plans usually have lower monthly premiums, but they may not cover all conditions or services. Pre‑existing conditions are often excluded.

Short‑term insurance can provide basic protection, but self‑employed individuals should carefully review what services are covered before choosing this option.

Health Savings Accounts and High Deductible Plans

High Deductible Health Plans (HDHP) have lower monthly premiums and higher deductibles. Paired with a Health Savings Account (HSA), self‑employed people can save money on taxes and pay for medical expenses with pre‑tax dollars.

Contributions to an HSA can reduce taxable income. HSA funds can be used for qualified medical expenses such as prescriptions, doctor visits, and certain treatments. HSAs are available only with eligible high deductible plans.

Health Insurance Options by Company

Different insurance companies offer plans that are suitable for self‑employed individuals. Costs and networks vary by state and plan type.

UnitedHealthcare

UnitedHealthcare offers a wide range of individual and family plans that can be purchased by self‑employed people. Plans include preventive care, telehealth services, and access to a large network of providers. UnitedHealthcare plans are available in many states.

Blue Cross Blue Shield

Blue Cross Blue Shield plans are available in every state through regional affiliates. Self‑employed people can choose from different plan options depending on their location. BCBS plans often include comprehensive coverage and access to many doctors and hospitals.

Cigna

Cigna offers individual health plans that may be suitable for self‑employed people who want flexible access to doctors and services. Cigna plans often include wellness programs and telehealth options.

Oscar Health

Oscar Health focuses on simplicity and user‑friendly tools. Its plans are designed for people who want an easy enrollment process and access to digital care features. Oscar Health plans are available in selected states.

Molina Healthcare

Molina Healthcare offers affordable plans in some states. These plans are often chosen by people who want low cost coverage. Molina may also provide access to Medicaid or marketplace plans depending on eligibility.

Tips for Choosing the Best Plan

Choosing the right health insurance plan as a self‑employed person requires careful comparison and understanding personal needs.

Assess Your Health Needs

Consider how often you visit doctors, whether you take prescription medications, and your general health. Plans with lower monthly costs may have higher out‑of‑pocket expenses when care is used.

Compare Networks

Make sure the plan’s network includes doctors and hospitals you prefer. Out‑of‑network care often costs more than in‑network services.

Review Total Cost

Look beyond monthly premium costs. Compare deductibles, copayments, coinsurance, and out‑of‑pocket maximums. A plan with a slightly higher monthly premium might save money overall if out‑of‑pocket costs are lower.

Consider Long‑Term Needs

If your income changes, family grows, or health needs change, you may need to reevaluate your plan during open enrollment. Planning ahead can help avoid unexpected costs.

Enrollment Periods for Self‑Employed People

Self‑employed individuals can enroll in marketplace plans during the annual open enrollment period. If you miss this period, qualifying life events such as marriage, birth of a child, or loss of previous coverage may allow a special enrollment window.

Common Questions About Self‑Employed Health Insurance

Can Self‑Employed People Get Subsidies?

Yes. Self‑employed individuals may qualify for premium subsidies if they purchase insurance through the marketplace and meet income requirements.

Are Short‑Term Plans a Good Idea?

Short‑term plans can be affordable, but they may not offer comprehensive coverage or protect against pre‑existing conditions.

Can Self‑Employed People Use HSAs?

Yes. Self‑employed people with high deductible health plans can use Health Savings Accounts to save money on taxes and pay for medical expenses.

Conclusion

Finding affordable and useful health insurance as a self‑employed person in the USA requires research, comparison, and understanding of plan details. Marketplace plans, subsidies, HSAs, and company options all play a role in choosing the best coverage. By reviewing your health needs, comparing plans, and knowing your costs, you can find a health insurance plan that works for your budget and protects your health in 2026.